$6.6 trillion. No, that’s not the national debt, it’s America’s Retirement Income Deficit [1] -- the cumulative amount Americans are lacking in retirement savings, according to the Center for Retirement Research [2].

The deficit, which amounts to $90,000 per household (aged 32-64), is a stark indicator of the US retirement system's woeful inadequacy. According to the Federal Reserve, only 53% of workers even have a retirement account, and those who do have a median balance of only $45,000 [3].

This inadequacy, sadly, is unsurprising. Little more than half of working Americans even have access to a retirement plan. For those fortunate ones, “do-it-yourself” 401k-style plans that offer little to no contribution from employers are by far the most common. And between stagnant wages, rampant unemployment, falling home prices, and skyrocketing healthcare costs, the average worker has very little to save for old age. Even those who manage to stash away a few dollars are far from safe; fees charged by the mutual funds in their retirement plans can gobble up nearly a third of their lifetime returns.

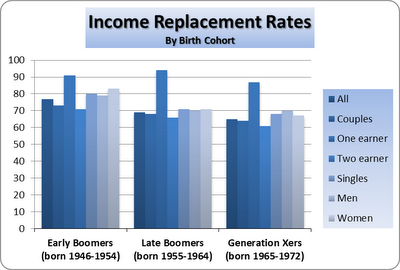

With all of these forces aligned, it’s no wonder workers’ retirement prospects are looking grim. Early baby boomers could expect a retirement income that was, on average, 77% [4] of what they earned during their peak earning years. Generation Xers, however, can expect to replace only 65% of their pre-retirement income -- 16% less than their parents.

It’s time to heed the call of Retirement USA [5], a coalition of organizations that commissioned the Retirement Income Deficit to create a new second tier of retirement options to replace the bygone pension system. Whatever form this solution takes, it must possess at least three qualities: universality, security, and adequacy.

In other words, this new plan must cover all workers (and be mandatory for those without other coverage), remain insulated against the risks of excessive fees and a turbulent market, and require employee, employer, and government contributions to ensure that all stakeholders contribute. And this solution must be implemented soon, before elderly poverty, which the creators of Social Security and many others have fought so hard to combat, begins to rise once again.

*Graph Source: “Retirements at Risk: The New National Retirement Risk Index” – CRR (2006)

This blog entry was written by Robbie Hiltonsmith of Dëmos [6]and is cross-posted on the Dëmos Ideas & Action blog [7].